What Offer Amount Should the Taxpayer Indicate in an Offer When There Is Doubt as to Liability?

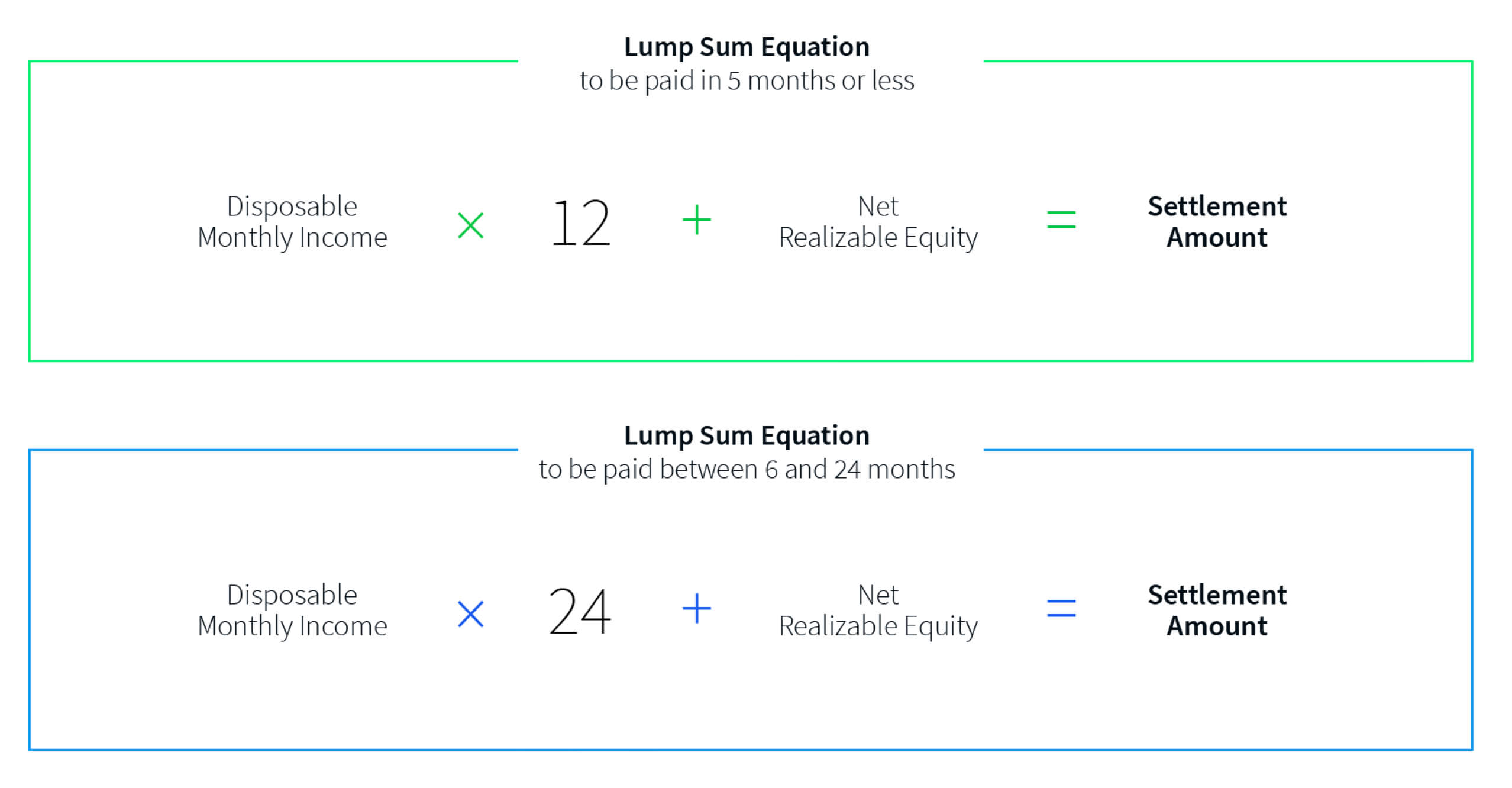

On the surface, a doubt as to collectibility offering in compromise looks fairly straightforward. The amount you offer is the product of a simple equation: But the technical numbers that go into an OIC offer calculation are just half of the story (if you're interested in a more technical treatment of OICs, you lot should check out our OIC ebook hither). When the IRS considers an OIC, they don't cease at the surface-level information you put on Form 433. They likewise scrutinize every slice of supporting documentation they can get their hands on—banking company records, credit card statements, holding valuations, medical records, and anything else that might be relevant. The IRS goes through all of this documentation line by line looking for anything that contradicts the story your offer tells. When they practise find a discrepancy, it throws up a blood-red flag. A unmarried discrepancy won't necessarily sink your offer, but it does put the IRS on alert. One time a red flag pops upwards, they're going to scrutinize your offering and documentation that much more, which only makes your job more difficult. So let'southward expect at two examples of real cases that got flagged during my fourth dimension at the IRS, and how you can help your OIC clients avert the aforementioned mistakes. The Case of the Mysteriously Undervalued Business firm I remember working one instance in conjunction with the Department of Justice where the individual owed about $150,000. 1 of the assets they reported was a home worth $1.6 one thousand thousand, verified past a realtor's valuation. However, later a little earthworks on our part, information technology became apparent that the valuation report from the realtor was incomplete. The written report didn't even list basic things like the number of bedrooms and bath in the abode. With a piddling more digging, we were able to more accurately value the house at $2 million, changing the individual'southward net realizable equity (NRE)—and therefore his ability to pay his taxes—substantially. I assume that no one reading this would intentionally misreport the value of their client's belongings. However, that'south not the only way a mistake similar this happens. A domicile's value could easily be under-reported (or even over-reported) considering of a lazy or uninformed valuation by a realtor. Similarly, an online tool such equally a Zillow "Zestimate" may provide inaccurate assessments in rural areas with limited market place information or in markets that are fluctuating significantly. If it is reasonable under the circumstances, your very all-time choice is a three-step procedure: Of form, this sort of double-documentation may not e'er be reasonable—or even possible. Fifty-fifty just a "Zestimate" can work as acceptable documentation for the value of your customer'south house if the value doesn't vary unreasonably from comparable homes in the area. Recollect, your job is to convince the IRS that the numbers yous put on the 433—your client's NRE in this case—are as accurate as possible. The Case of the Very Expensive Steaks I worked some other case every bit a Revenue Officer where the taxpayer claimed that they couldn't pay their tax debt, in function, for medical reasons. The taxpayer had a cardiac condition that had led to a heart attack, and treating that condition was expensive. On the surface, information technology seemed to exist a compelling example. If everything was every bit this taxpayer claimed, the additional medical costs would have left him with little to no dispensable monthly income. With no disposable monthly income, this OIC would very likely accept been accepted and the taxpayer'due south debt settled. And then when you're going over a customer'southward case, brand certain the tax was assessed correctly. Did the IRS follow all the right procedures when assessing the tax? Did they assess the tax within the assessment statute of limitations? Maybe the IRS assessed a trust fund tax against a person who didn't meet the criteria of willfulness or responsibility. If you tin can show that the IRS didn't assess your customer's taxation by the book, you tin can brand a good case for a DATL OIC. Effective tax administration isn't as easy to define every bit either doubt as to liability or doubtfulness equally to collectibility. That'due south because ETA cases are the "everything else" category of the OIC world and tin can just be considered once DATL and DATC accept been ruled out every bit options. In other words, ETA is for those unique cases when the taxation has been assessed correctly and the taxpayer tin technically beget to pay, but there'due south still a adept reason why they shouldn't. Only why would the IRS ever accept an offering if the taxpayer can afford to pay and the tax was assessed correctly? Well first, because Congress told them to. As a part of the IRS Restructuring and Reform Act of 1998, Congress instructed the Service to consider policies that encourage taxpayers to comply with the taxation laws because "they believe the laws to exist fair and equitable" (IRM five.8.11.1). Essentially, Congress believed that more people would be willing to pay their taxes if they saw that the IRS is able to brand exceptions in extreme circumstances. Simply likewise Then that's the driving principle behind an ETA OIC: what outcome is going to expect good for anybody involved? Allow me requite you some other instance. I worked a instance involving a taxpayer who made a living running a daycare. They owed dorsum taxes and were facing the possibility of having their home and bank accounts seized if they didn't cooperate. Also, this taxpayer recently lost both artillery, had been hospitalized for In this case, what looks good for everyone? The taxpayer'south offer was accepted, and their IRS debt was one less affair they had to worry about. During my time as a Acquirement Officer at the IRS, I saw a lot of niggling mistakes on OIC forms that had large impacts on cases. Sometimes these mistakes would simply cause confusion and stall the case until the fault could be clarified. Sometimes the mistakes were enough to get the offer rejected outright. Either result is time-consuming and costly for both you and your clients. Let's go over a few of these simple mistakes, why they matter, and the easiest way you can make certain they don't happen to yous. Unfortunately, when that ball does get dropped—a quick-sale value is calculated incorrectly, or an expense is included in the wrong calculation—the whole OIC process has to come up to a screeching halt until the error is sorted out. There are a couple means yous tin can go about making certain these kinds of mistakes don't happen on your offers. Yous could hire someone to obsessively pour over every facet of your return, recalculate always calculation and double bank check every grade field for accuracy. You certainly don't accept time to do every offer twice. Or you can use tax resolution software to practise all that for yous. I can't speak specifically to other revenue enhancement resolution software, but I know that Awning solves each of the problems I've outlined hither. When yous use Canopy to prepare your OIC, our software does all of the computing for y'all, brand sure yous don't go out whatever blank fields, and helps you comply with IRS standards. Non simply does that relieve you time Simply as importantly, Canopy frees you upward to worry about more important things than exactly how to comply with every nuanced IRS standard. How you spend that time—edifice client relationships, growing your practice, or perfecting your golf swing—is upwardly to yous.

Doubtfulness as to Collectibility: When the Taxpayer Can't Pay

ETA: Good PR and Everyone'southward Happy

Who Will Non Authorize for Offer in Compromise?

Y'all probably wouldn't await this, but I saw a lot of bad math from tax pros during my time at the IRS. Not because CPAs and EAs are bad at math, just because perfectly filling out a form 433 is hard. It requires juggling dozens of circuitous numbers and figures, not to mention all the explanations and supporting documentation that accompany the numbers. It'southward no wonder the brawl gets dropped sometimes.

When I saw an empty field on a 433 or 656 (something I saw far too frequently), there was no way for me to know why the practitioner had left information technology blank. Was information technology blank considering it didn't use to the taxpayer? Considering they didn't understand how to reply? Or was I missing data crucial to the case and the taxation pro made a unproblematic mistake? I had to know the answer earlier I could proceed with my recommendation on the offer. It'due south a shame that something so small tin can hold up such an of import decision, but I saw it happen often.

This is some other mistake I saw frequently: when a taxpayer's property was worth less than they owed on it, the preparer would often subtract that negative equity from the taxpayer'southward net realizable equity (NRE). You tin can't practise that, helpful as it may seem to your client's case. Any asset with negative disinterestedness should have a reported disinterestedness of zero.

The Best Mode to Fill up Out OIC Forms

Source: https://www.getcanopy.com/offer-in-compromise-guide

0 Response to "What Offer Amount Should the Taxpayer Indicate in an Offer When There Is Doubt as to Liability?"

Post a Comment